July 2, 2026

PJM’s Record-Breaking Demand Highlights Tight Reserve Margins

By: Bob Barron, VP, Energy Management at Competitive Power Ventures (CPV)

- PJM opened its Base Residual Auction on June 30th for contract year 2028/2029 with very little suspense on expected pricing given the continued existence of the collar (floor/$175 and cap/$325).

- The auction closes on July 7, and results will be posted on July 14, while PJM remains focused on securing additional resources outside of the normal auction timeline.

- PJM was unable to procure sufficient resources in the previous auction, which led them to initiate a Reliability Backstop Program in the hopes of closing a 6.6 GW gap.

NYISO Regulatory Review

- The NYISO asked customers to conserve power usage through this recent heat dome, which has elevated demand above 30,000 MW while also pushing real-time prices above $400/MWH.

- The recently activated Champlain-Hudson Power Express power line has not been delivering any power during the recent extreme conditions.

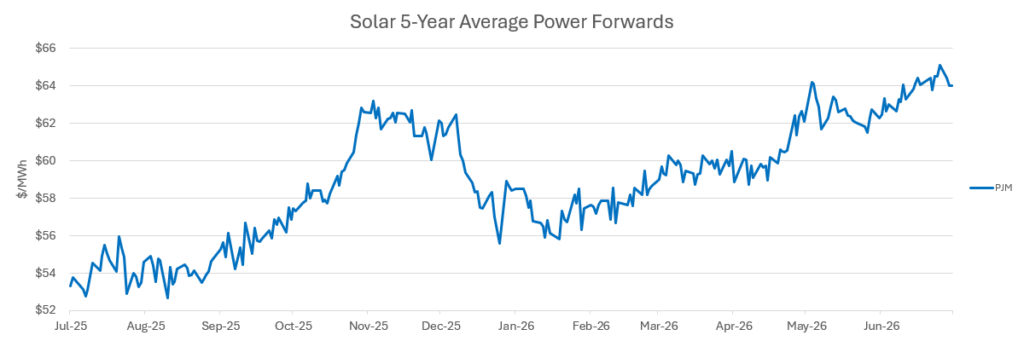

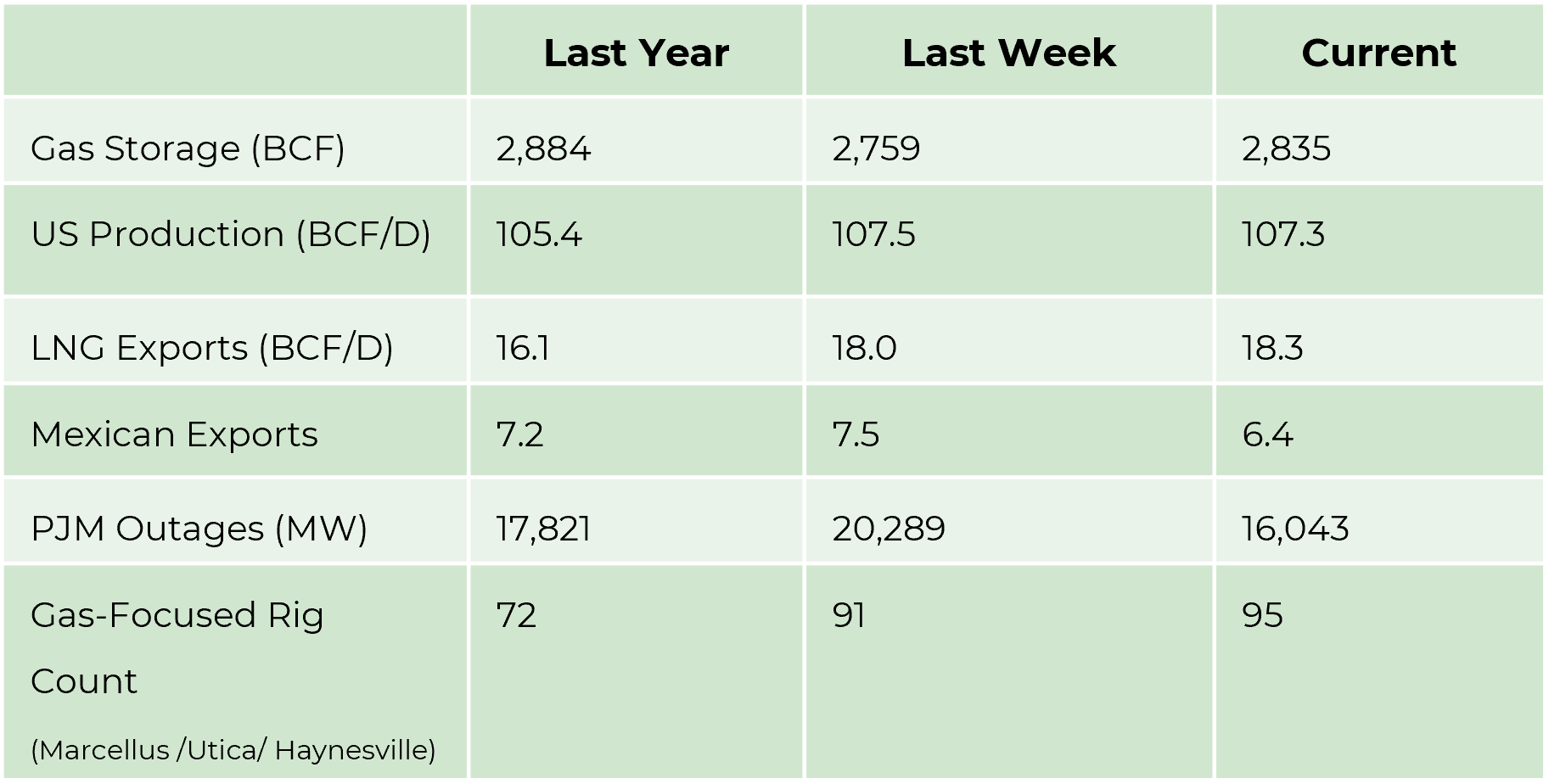

Market Drivers

Market Drivers as of July 2, 2026.

- Gas Storage/Year over year difference. A positive number is bearish, and a negative number is bullish.

- Production /Year over year growth/trend is important in the context of demand growth.

- LNG Exports/Year over year growth means demand is growing and should be looked at in comparison to production trend.

- Mexican Exports/Add to LNG Exports to show a trend in exports compared to the production trend.

- PJM Outages- generally seasonal in Spring or Fall/Can support short-term prices.

- Gas Focused Rig Count/Is drilling increasing to grow production versus demand growth. This can be seen as impacting price in the future based on expected load growth.

Energy Market Update

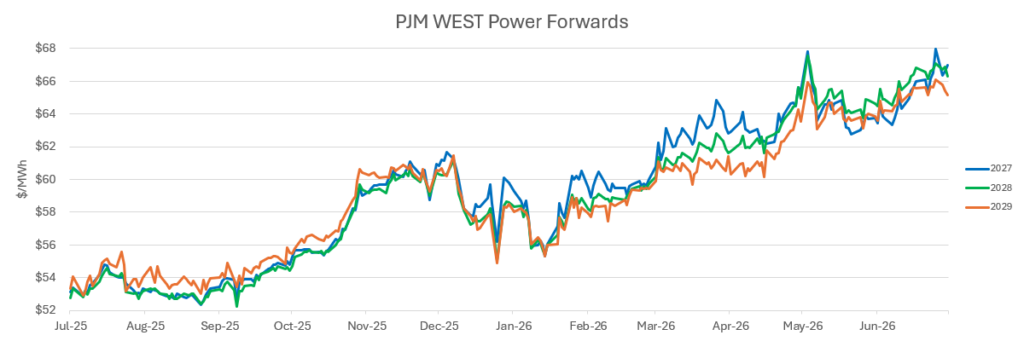

- PJM experienced a record for peak demand yesterday as load reached 162,200 MW during the heat wave currently enveloping the eastern US. That record is not expected to last long, as today’s forecast is expected to reach 166,000 MW.

- Power prices reacted accordingly as on-peak prices traded at just under $600/MWH and real-time prices exceeded $1500/MWH at several trading hubs.

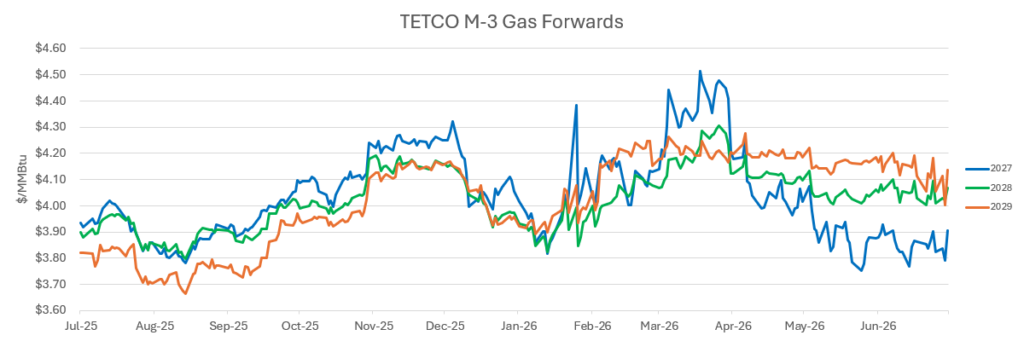

- While gas prices remained subdued across most of the grid, increased demand in New York and New England spiked Iroquois Zone 2 prices to $14/MMBTU for at least one package as imports from Canada were necessary to satisfy gas-fired power demand.

- Total gas-fired power demand reached just under 50 BCF/D over the recent heat wave, which left no net supply available for storage injections and likely required some withdrawals from peaking facilities in the south.

- Delivery times for critical equipment like transformers and turbines continue to elongate, thus putting additional risk in the coming generation build-out to support load growth based on expected data center demand.

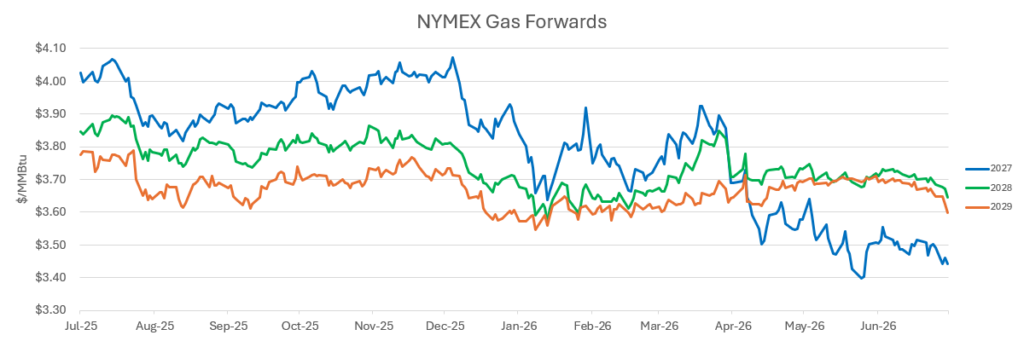

- Calendar/2027 NYMEX is trading near the lows of the contract near $3.40/MMBTU as storage levels are expected to reach 3.9 TCF heading into the coming winter, and supply from associated gas out of the Permian Basin is expected to rapidly increase as new egress capacity enters service.