March 20, 2026

U.S. Natural Gas Market Drivers: Current Conditions and Outlook

By: Bob Barron, VP of Energy Management, CPV

U.S. natural gas prices remain largely driven by strong domestic supply and storage conditions despite global LNG disruptions, though rising export capacity and sustained international demand may place upward pressure on prices in the coming months.

- PJM recently announced that transmission capacity availability will be adjusted for ambient temperature conditions on an hourly basis. This change had been proposed originally under FERC Order 881, issued in 2021, and could expand capacity without a significant capital requirement.

- PJM is still expecting the FERC to adopt proposed tariff revisions related to Retail “behind-the-meter-generation” (BTMG) by May 28, 2026, so the new rules will be effective by July 31, 2026.

NYISO Regulatory Review

- New York regulators and legislatures continue to review options to deal with expected load growth and how that balances with environmental goals and date certain carbon intensity promises.

- Recent gas price volatility which led to significant fuel switching has highlighted the possible need for new infrastructure to help mitigate the growing winter peak demand forecasts and the end-of-pipeline volatility exhibited during Winter Storm Fern.

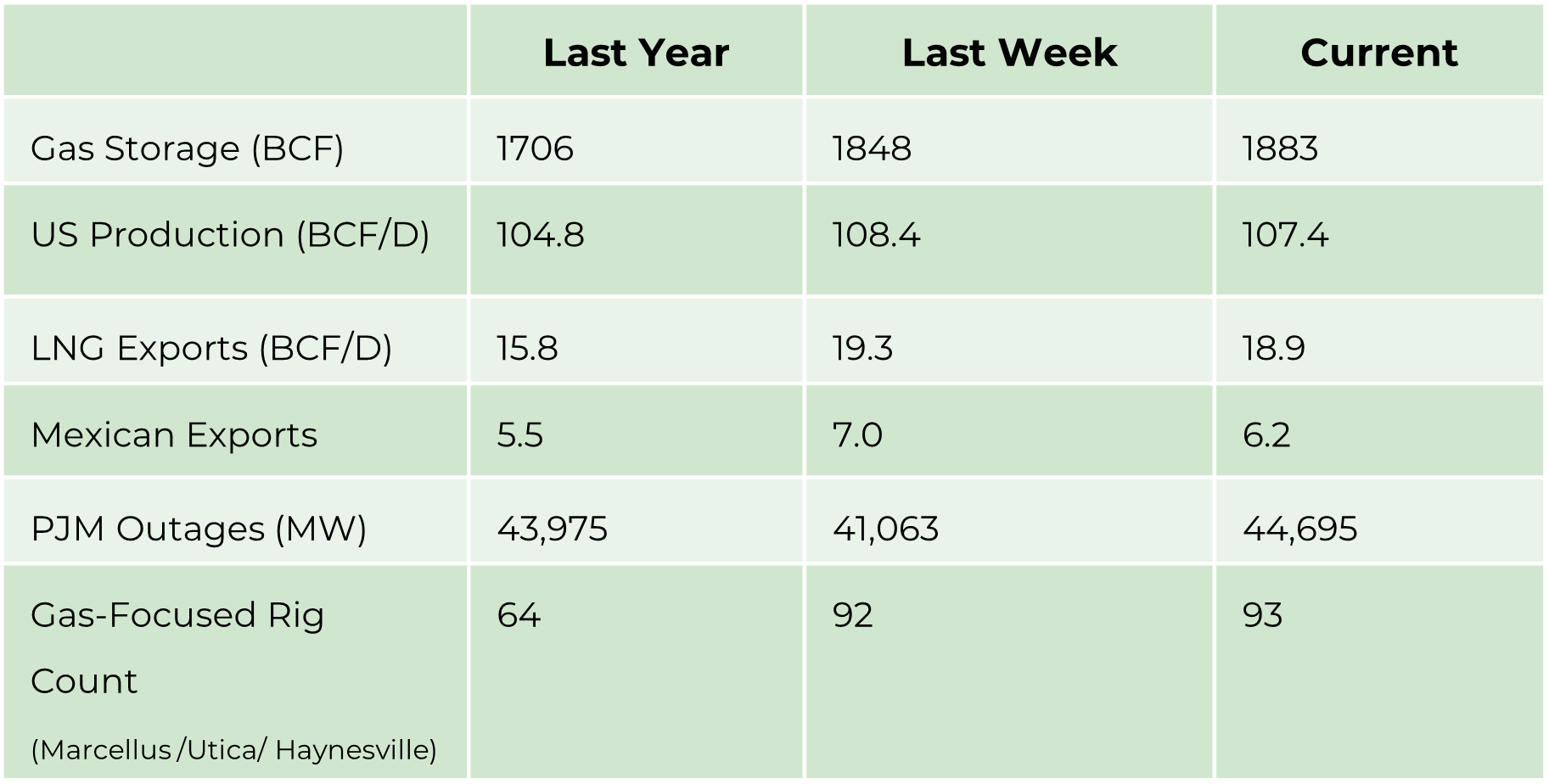

Market Drivers

- Gas Storage/Year over year difference. A positive number is bearish, and a negative number is bullish.

- Production /Year over year growth/trend is important in the context of demand growth.

- LNG Exports/Year over year growth means demand is growing and should be looked at in comparison to production trend.

- Mexican Exports/Add to LNG Exports to show a trend in exports compared to the production trend.

- PJM Outages- generally seasonal in Spring or Fall/Can support short-term prices.

- Gas Focused Rig Count/Is drilling increasing to grow production versus demand growth. This can be seen as impacting price in the future based on expected load growth.

Energy Market Update

- Events unfolding in the Middle East continue to dominate the news as oil prices exploded higher and reached $120/BBL before settling back to current trading levels straddling $100/BBL with up and down movements based on the most recent headline.

- Domestic natural gas prices are well insulated from global events as the U.S. is maxed out on LNG exports, while awaiting the completion of Golden Pass’s commissioning efforts, which is expected by the end of Q2.

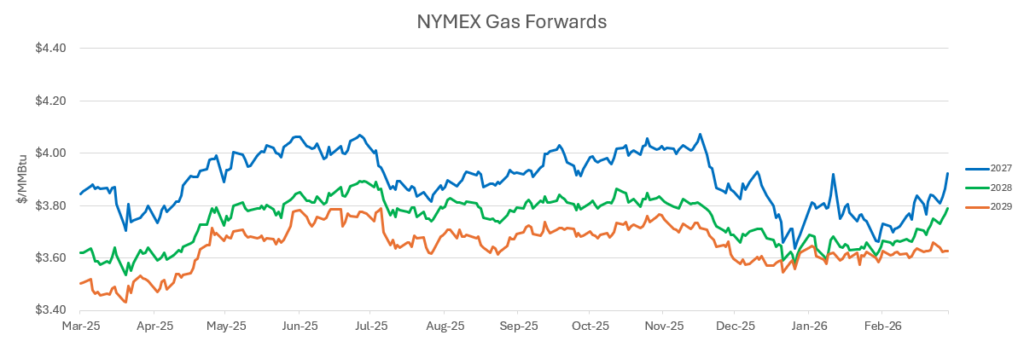

- Moderate weather this past week will be followed by colder than normal conditions this week has storage operators going from injections to withdrawals as winter draws to a close. Weak cash prices (Marcellus slightly above $2.0/MMBtu) has kept April NYMEX prices in check with some back and forth between $3.0-$3.25/MMBtu.

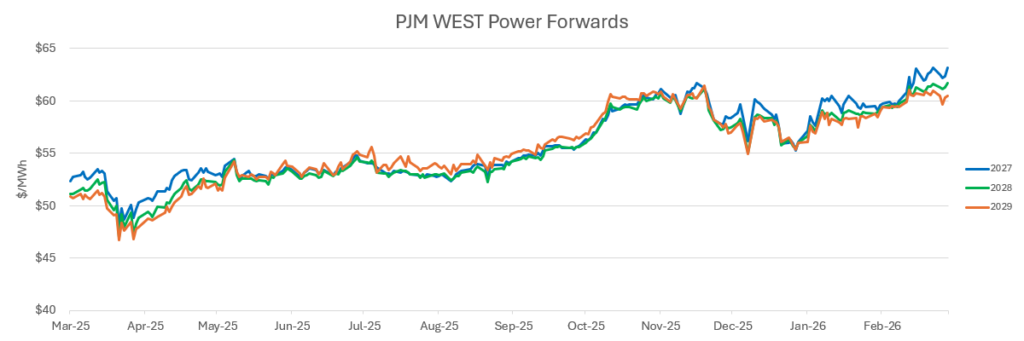

- Power demand growth continues to be the main topic of discussion as speed-to-market data center focused generation requirements have collided with the politics of rapidly rising power prices affecting consumers. Data centers are now being asked to bring their own generation solutions, which minimize the impact on existing retail customers.